IRS penalties can quickly increase the amount you owe if you file late, pay late, or underreport income, often adding monthly charges and interest until the balance is resolved. The Internal Revenue Service assesses these penalties to encourage timely and accurate tax compliance, but in some cases, they may be reduced or removed through options like reasonable cause relief or first-time penalty abatement. If you’re facing a notice or growing balance, understanding how these penalties work and when to seek professional IRS representation can help you take the right steps to minimize the financial impact.

Quick Overview: IRS Penalties and How to Reduce Them

✓ The Internal Revenue Service may charge penalties for filing late, paying late, underpaying estimated taxes, payroll deposit issues, inaccuracies, or fraud, with penalties often accruing monthly plus interest.

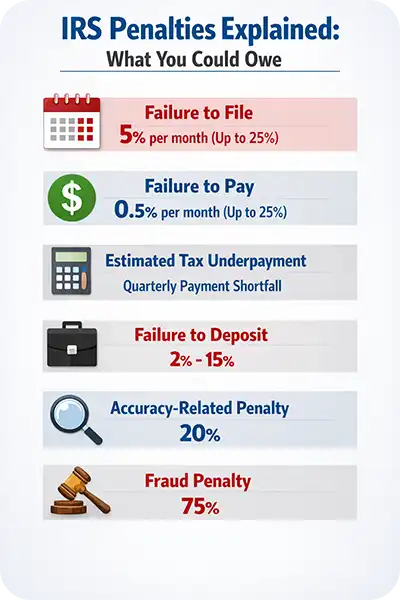

✓ The most common penalties include failure to file (up to 25%), failure to pay (up to 25%), estimated tax underpayment, failure to deposit (2% to 15% for businesses), and accuracy-related penalties (20%).

✓ Filing your return on time, even if you can’t pay, can significantly reduce how much you owe in penalties.

✓ Some penalties may be reduced or removed through reasonable cause relief or First-Time Penalty Abatement (FTA) if you qualify.

✓ You can request relief by contacting the IRS directly or filing Form 843, and in complex cases, professional IRS representation can help minimize long-term financial impact.

Common Types of IRS Penalties

The IRS imposes several different types of penalties, each one depending on the nature of the issue. Some apply to individuals and their personal tax return, while others may primarily affect business owners or self-employed individuals. Some of the most common penalties and interest fees include the following.

Failure to File Penalty

The failure to file penalty applies when you do not submit your tax return by the filing deadline (including extensions). A failure to file your tax return is one of the most severe and fast-growing penalties you can incur. Generally speaking, if you do not submit your taxes on time, the IRS charges:

✓ 5% of the unpaid taxes per month, applied for each month (or part of a month) that your return is late

✓ Capped at 25% of your unpaid tax balance

If your return is more than 60 days late, the IRS may impose a minimum penalty amount, even if you owe little or no tax. One thing that’s important to understand is that filing your return, even if you can’t pay your tax bill, typically reduces overall penalties. The failure to file penalty is significantly higher than the failure to pay penalty.

Failure to Pay Penalty

Not paying tax obligations also results in a penalty. The failure to pay penalty applies when you file your return but do not pay the taxes owed by the deadline. The IRS typically charges:

✓ 0.5% of unpaid taxes per month

✓ Capped at 25% of the unpaid amount

If both failure to file and failure to pay penalties apply in the same month, the failure to file penalty is reduced so the combined rate does not exceed 5% per month. If you set up an installment agreement, the penalty rate may be reduced while the agreement remains active.

Estimated Tax Underpayment Penalty

Some individuals need to pay quarterly taxes throughout the year in order to avoid penalties when it’s time to file. This helps you meet your tax obligations and avoid a large bill at the end of the year. Typically, this is for self-employed individuals, freelancers, contractors, gig workers, small business owners, or other eligible individuals. If you’re not sure whether you owe quarterly payments, it’s best to seek tax advice from a professional.

If you do not pay enough tax throughout the year through withholding or quarterly estimated payments, the IRS may assess an underpayment of estimated tax penalty. The penalty is calculated based on:

✓ How much you underpaid

✓ How long the amount remained unpaid

✓ The IRS interest rate for that quarter

Many taxpayers can avoid this penalty by meeting safe harbor rules, such as paying at least 90% of the current year’s tax or 100% (or 110% for higher earners) of the prior year’s tax liability.

Failure to Deposit Penalties

Businesses that withhold payroll taxes may also face penalties if they do not deposit the withholdings with the IRS. The estimated tax penalty for this is typically between 2% and 15% of the unpaid amount, depending on how late the deposit is. You can find more information about this here.

Accuracy-Related Penalty

The accuracy-related penalty applies when the IRS determines there was a substantial understatement of tax or negligence in reporting. This penalty is generally 20% of the portion of tax underpaid, and typically does not trigger fraud-related issues. However, it’s important to resolve the penalty quickly to avoid further problems.

Fraud Penalties (Civil vs. Criminal)

The fraud penalty is significantly more serious and applies when the IRS believes a taxpayer intentionally attempted to evade taxes. The penalty is usually 75% of the portion of underpayment attributable to fraud.

Fraud penalties require evidence of intentional misconduct and are rare compared to other penalties. Still, they can be financially devastating, and, in extreme cases, may lead to criminal prosecution.

Why Did the IRS Charge Me a Penalty?

As mentioned above, there are several reasons that the IRS may charge you a penalty. Typically, you will receive a formalized notice or letter from the IRS that outlines the reason and any additional taxes you owe, including penalties and fines. To reduce the likelihood of compounding penalties, it’s recommended to pay the full amount. If you can’t pay the full amount, there are a few options that you can take, such as setting up a payment plan or disputing a penalty.

Can IRS Penalties Be Reduced or Removed?

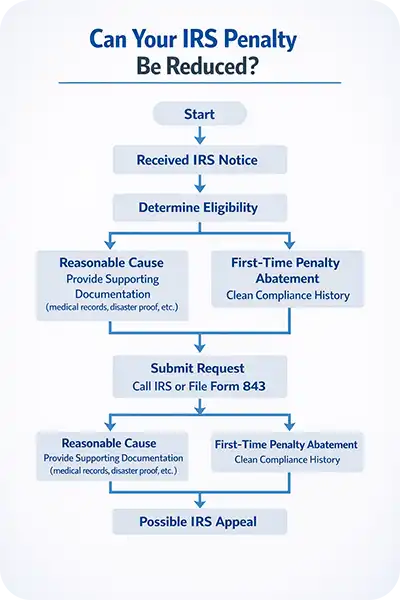

You can avoid a penalty by filing your tax return on time, in addition to making accurate estimated tax payments throughout the year. However, according to the IRS website, they may also be able to remove or reduce some penalties if you acted in good faith and can show reasonable cause for why you were not able to meet your tax obligations. Some examples of reasonable cause include:

✓ Serious illness, hospitalization, or medical emergency affecting you or an immediate family member

✓ Death of a spouse, parent, child, or other close family member near the filing deadline

✓ Natural disasters such as hurricanes, wildfires, floods, or earthquakes that disrupted records or access

✓ Destruction or loss of tax records due to fire, theft, flood, or cyberattack

There are additional circumstances where you may be able to get penalties removed for individual or business tax payments, but the types of penalty relief vary based on unique circumstances. For more information, partner with a certified public accountant.

First-Time Penalty Abatement (FTA)

First-time penalty abatement is an administrative relief option offered by the IRS that allows eligible taxpayers to have certain penalties removed if they have a clean compliance history. To qualify, taxpayers generally must have filed all required returns, paid or arranged to pay any taxes owed, and have no significant penalties in the prior three years. If approved, the IRS may remove the qualifying penalties along with related interest, which can substantially reduce the overall tax balance.

Penalty Appeal

Some taxpayers may also be eligible to request an IRS Independent Office of Appeals conference or hearing. This is typically only possible 30 days from the date of the rejection letter to file your request for an appeal, if certain circumstances have occurred, as outlined here. You can also work with a tax professional to determine your penalty appeal eligibility.

How to Request IRS Penalty Relief

You can request relief by calling the IRS directly, submitting a written request, or filing Form 843 (Claim for Refund and Request for Abatement) if applicable. In your request, clearly explain the reason you’re seeking relief, whether it’s reasonable cause, first-time penalty abatement, or another qualifying circumstance, and include supporting documentation, such as medical records, disaster reports, or proof of corrected compliance.

When to Seek Professional Help

Receiving a notice or letter from the IRS can be a bit intimidating, especially if you weren’t expecting it. And, while the IRS notice should contain information about the interest or penalty, it can still be challenging to understand the next step action items. To help ensure that you get your tax obligations sorted, pay a fine, or request penalty relief, working with a professional tax advisor is recommended. If you need help navigating penalties or your taxes in general, contact the professionals at Del Real Tax today.