Falling behind can feel overwhelming, but knowing how to file back taxes is the first step toward regaining control. With the right strategy and guidance from a professional trained in certified tax coach planning, you can catch up, reduce penalties, and create a clear path forward. Here, we’ll provide a basic overview of how to file back taxes and set up a payment plan.

Key Takeaways: Quick Steps to File Back Taxes

Back taxes are unpaid federal or state taxes from a prior year, and they begin accruing penalties and daily compounding interest immediately after the filing deadline passes.

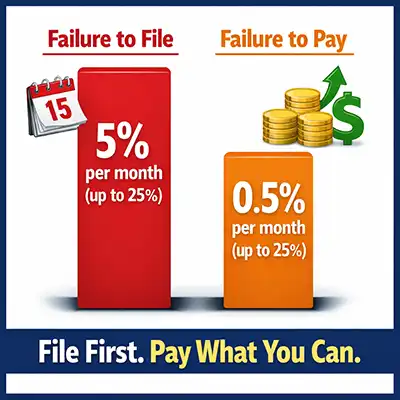

Failing to file is more expensive than failing to pay. The failure to file penalty can reach 25% of your unpaid taxes, and unresolved balances may lead to tax liens, levies, or wage garnishment.

You can file back taxes at any time, but refunds are only available within three years of the original deadline. The IRS typically requires the last six years of returns to consider you compliant.

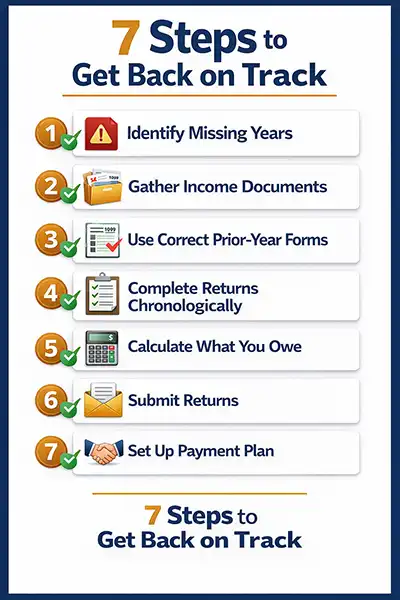

Filing back taxes follows a clear step-by-step process: identify missing years, gather income documents, use the correct prior-year forms, file each return accurately, and calculate what you owe.

If you can’t pay in full, payment plans and relief options are available. Filing first opens the door to installment agreements and other tax resolution strategies, especially with guidance from a qualified tax professional.

What Are Back Taxes?

Back taxes are state or federal taxes that were not paid by the original filing deadline; anything you owe from a previous year that is still unpaid. They can happen for a few different reasons. Some of the most common include:

✓ You didn’t file a tax return at all

✓ You filed a return but didn’t pay the full amount owed

✓ You underreported your wage and income, and now owe additional tax after an adjustment

If a tax balance remains unpaid after the deadline, it becomes past-due tax debt, and the IRS (or your state tax agency) begins adding penalties and interest until the balance is resolved.

When Do Taxes Become “Back Taxes”?

If you don’t file your return by the IRS due date, they’re considered back taxes the next day. That means you need to file by April 15 (or the adjusted date if applicable), and if you don’t, the IRS starts to charge penalties and interest beginning April 16. Even if you’re owed a tax refund, failing to file still counts as an unfiled return, and you only have a limited time to claim that refund. However, it’s not uncommon for people to miss the tax filing deadline, and, as long as you act quickly, you can reduce the risk of severe penalties.

Federal vs. State Back Taxes

It’s also important to understand that federal and state tax debts are separate.

✓ Federal back taxes are handled by the Internal Revenue Service (IRS).

✓ State back taxes are handled by your state’s department of revenue or taxation agency.

If you owe both, you’ll need to address each separately, including filing overdue returns and potentially setting up two different payment plans.

What Happens If You Don’t File Taxes?

There are two main penalties that you incur if you don’t file your taxes: failure to file and failure to pay. Interest will also start to accrue on any unpaid balance for the tax year.

Failure to File Penalty: Generally, 5% of unpaid taxes per month (up to 25%) if you don’t submit your return on time. This penalty grows quickly and is typically higher than the failure-to-pay penalty.

Failure to Pay Penalty: Usually 0.5% of the unpaid balance per month (up to 25%) if you file but don’t pay what you owe.

Interest on Back Taxes: The Internal Revenue Service (IRS) charges daily compounding interest on unpaid taxes and, in some cases, on penalties, until the balance is paid in full.

Tax Lien: If the debt remains unresolved, the IRS may file a federal tax lien, which is a legal claim against your property and can affect your credit and ability to sell or refinance assets.

Levies and Wage Garnishment: In more serious cases, the IRS can issue a levy to seize funds from your bank account, garnish wages, or take certain assets to satisfy the tax debt.

How Many Years Can You File Back Taxes?

Technically, you can file a past-due tax return at any time. There’s no strict deadline that permanently prevents you from submitting an old return. However, there are important time limits, especially if you’re owed a refund.

The Three-Year Refund Rule

If you’re due a refund, the IRS generally gives you within three years of the tax deadline to claim it. For example:

✓ If you didn’t file your 2021 return (originally due in 2022), you typically have until 2025 to claim a refund.

After that three-year window, you can still file the return (and you should), but you forfeit the refund.

How Far Back Does the IRS Require You to File?

While there’s no statute of limitations on filing a return that was never submitted, the IRS typically requires taxpayers to file the last six years of returns to be considered compliant. If you haven’t filed in many years, the IRS may:

✓ Request specific missing years

✓ File a Substitute for Return (SFR) on your behalf

✓ Require multiple years before approving a payment plan

Filing voluntarily before enforcement action begins usually gives you more flexibility and options.

Step-by-Step Guide on How to File Back Taxes

If you’re behind on taxes, it’s important to file them as soon as possible to avoid continued fines and compounding interest. For those with complicated tax forms or questions about deductions and credits, disability benefits, and more, it’s best to work with a professional tax preparer. Otherwise, consider the following steps to help with back tax preparation and filing.

Step 1: Figure Out Which Years You Need to File

Start by identifying every year you missed.

✓ Check your IRS account transcript or request a wage & income transcript

✓ Look for IRS notices (they’ll list tax years in question)

✓ Confirm whether your state also requires a return for those years

If you’re unsure, you can pull wage and income transcripts directly from the IRS website to see what income was reported under your Social Security number.

Step 2: Gather Your Income Documents

You’ll need records for each unfiled year, along with key tax documents. Some of the most important ones necessary for filing your tax returns include:

✓ W-2s (employment income)

✓ 1099 forms (contract, freelance, gig work)

✓ 1099-INT / 1099-DIV (interest & dividends)

✓ Business income/expense records (if self-employed)

If you’re missing deduction records, gather bank statements, mortgage interest statements, tuition records, or charitable receipts where possible.

Step 3: Get the Correct Prior-Year Tax Forms

You must use the forms for the specific tax year you’re filing, not the current year’s version. For example:

✓ Prior-year Form 1040

✓ Schedules A, B, C, etc., if applicable

Older returns often must be mailed. Some tax software providers allow you to file electronically for recent prior years, but most older returns are paper-filed.

Step 4: Complete One Year at a Time

If you have multiple prior-year returns that you need to complete, work chronologically, starting at the oldest year. This is important because:

✓ It prevents confusion with carryovers (like losses or credits)

✓ Some balances affect future years

✓ The IRS may require your prior-year income tax returns before approving a payment plan

Be accurate and complete. Filing incorrectly can trigger additional notices or delays. If multiple years are involved, label and mail each return in a separate envelope unless instructed otherwise. You can use the IRS Free File option if applicable, but it may be best to work with a CPA to ensure you have everything in order.

Step 5: Calculate What You Owe (Including Penalties)

Once returns are prepared, determine:

✓ Tax owed

✓ Failure-to-file penalty

✓ Failure-to-pay penalty

✓ Accrued interest

The IRS will calculate exact penalties after processing, but estimating helps you prepare. Keep in mind that the failure to file penalty is typically much higher than the failure to pay penalty, so it’s worth having filed tax returns on record even if you can’t pay immediately.

Step 6: Submit Your Back Tax Returns

Mail each completed return to the address listed for that tax year (these differ by state and whether payment is included). If possible, try to send it by certified mail, as this will provide you with verification that it’s been delivered. Since processing federal income returns may take several weeks, sometimes longer, it’s good to have the peace of mind knowing that it arrived in the right place.

Step 7: Pay in Full or Set Up a Payment Plan

If you can pay the full balance of past-due returns, interest stops accumulating once paid. If you can’t pay, you can apply for:

✓ A short-term payment plan

✓ A long-term installment agreement

✓ Other tax relief options

You can request a tax payment installment agreement directly through the IRS online system once your returns are processed. Additionally, you may be eligible for a payment plan or an offer in compromise, depending on qualifications and earned income, but it’s best to work with a professional in these types of tax situations.

When to Hire a Tax Professional

For the best outcomes, it’s important to submit state and federal tax returns when it’s time to file based on the IRS deadlines each year. However, if you’re having trouble with your taxes or aren’t sure if you’ve been staying compliant, working with a tax professional is recommended. Book a demo with Del Real Tax today to ensure optimal tax return preparation and get help with any back taxes you may have.